65% of This Year's New Launches Are in the Suburbs. That's Not a Coincidence.

For years, the narrative was simple. CCR condos were for the rich. RCR was the “sweet spot.” And OCR? That was where you went if you couldn’t afford anything else.

That story’s done.

In 2026, roughly 65% of all new private launches will be in the Outside Central Region. That’s not some gradual shift. That’s the suburbs taking centrestage, and the numbers are too big to ignore.

The lineup

Let’s talk about what’s actually coming.

Bayshore Road GLS is bringing 815 units to a precinct that’s never had private condos before. First-ever private homes in Bayshore. Tengah Garden Residences (860 units) is doing the same for Tengah, Singapore’s “forest town.” And Hougang Central just got awarded to a CapitaLand-UOL consortium for $1.5 billion, an integrated development with 835 units sitting right on top of Hougang MRT, which will serve both the North-East Line and the upcoming Cross Island Line.

Narra Residences at Dairy Farm launched in February at an average $2,180 psf and moved about 25% on opening weekend. Pinery Residences at Tampines is another mixed-use project with 588 units. Then there’s a 575-unit CDL project at Lakeside Drive and Kingsford’s 500-unit project at Lentor Gardens.

That’s over 4,000 suburban units hitting the market this year. Compare that to the 4,040 OCR units launched in all of 2025.

The price gap is real

Here’s where it gets interesting.

OCR new launches are pricing at $1,800 to $2,300 psf. RCR sits at $2,400 to $2,800 psf. CCR? $2,800 and above, easily north of $3,200 for anything decent.

When River Modern sold 90% at $3,266 psf average, people cheered. But that’s a 1-bedder starting around $1.3 million. A 3-bedder there is comfortably north of $3 million.

Meanwhile, at Narra Residences, a 2-bedder starts from $1.176 million. A 3-bedder from $1.63 million. In a brand new development. Near nature reserves.

The math isn’t even close.

Why developers are going suburban

It’s not just about land availability. Developers are reading the room.

The unsold inventory across Singapore sits at 14,859 units, the lowest in 15 quarters. But the demand isn’t uniformly distributed. The February 2026 BTO exercise told the real story: Tampines projects were 8x oversubscribed (6,277 applicants for 539 flats), while Toa Payoh’s first Plus project drew a lukewarm 1.7x application rate.

People want space. They want proximity to their parents. They want to not spend $3 million on a 3-bedder.

And with SORA sitting at around 1.12% (a 3-year low), monthly mortgage payments on a $1.5 million OCR condo are actually manageable. Fixed rates at 1.3% to 1.5% make the sums even friendlier. (If you missed our breakdown on that, here’s the piece on SORA and mortgage decisions.)

The emerging precincts to watch

Three precincts are getting private residential for the first time:

Bayshore is the one I’m most curious about. It’s the stretch along East Coast between Bedok and Tanah Merah, with the Thomson-East Coast Line already running through. The 815-unit Bayshore Road GLS project will be the test case for whether this neighbourhood can command a premium. My guess: it will, eventually. East Coast adjacent with MRT access is a strong proposition.

Tengah still feels early. The “car-free town centre” narrative is compelling on paper, but the estate is still very much under construction. The 860-unit Tengah Garden Avenue project by Hong Leong, GuocoLand and CSC Land will be priced aggresively, but you’re buying the future here, not the present.

Hougang Central might be the sleeper hit. The $1.5 billion CapitaLand-UOL integrated hub will have 835 residential units, plus retail, a bus interchange, and dual MRT line access (with Cross Island Line coming by 2030). Integrated developments in Singapore have historically outperformed their standalone neighbours. Think The Woodleigh Residences, Northshore Plaza, Punggol Digital District.

What this means for you

If you’re a buyer or upgrader looking at the next 2 to 3 years, the suburban pipeline is genuinely interesting. You’re getting brand new precincts with modern infrastructure, MRT connectivity that didn’t exist 5 years ago, and pricing that’s 30 to 40% below RCR equivalents.

The catch? You’re buying into the vision. Bayshore doesn’t have the cafes yet. Tengah doesn’t have the mature trees. Hougang Central’s integrated hub won’t complete until 2030 or 2031.

But that’s also where the upside lives.

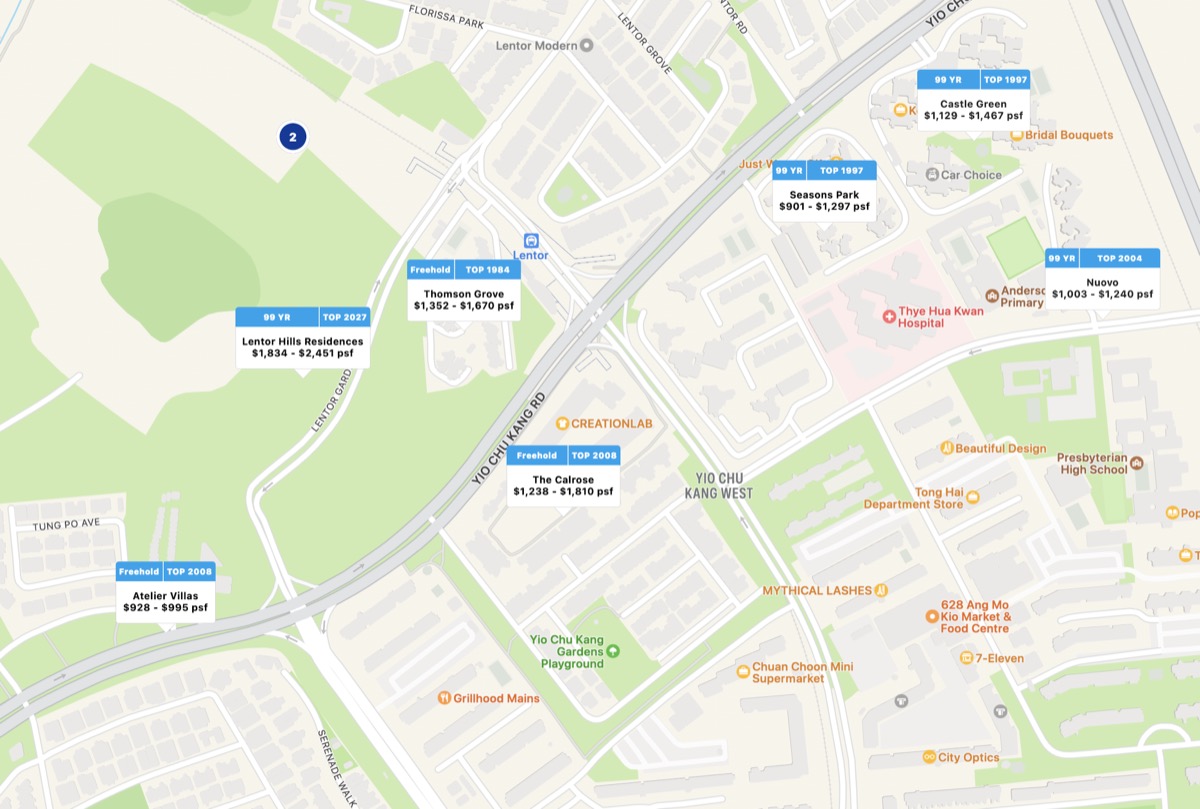

The last time a new precinct got its first wave of private homes, we saw significant appreciation once the area matured. The Lentor corridor is a recent example; Lentor Modern, Lentor Hills Residences, and Lentoria created their own little ecosystem, and prices have held firm.

2026 isn’t about the CCR anymore. The suburbs aren’t the backup plan. They’re the main event.