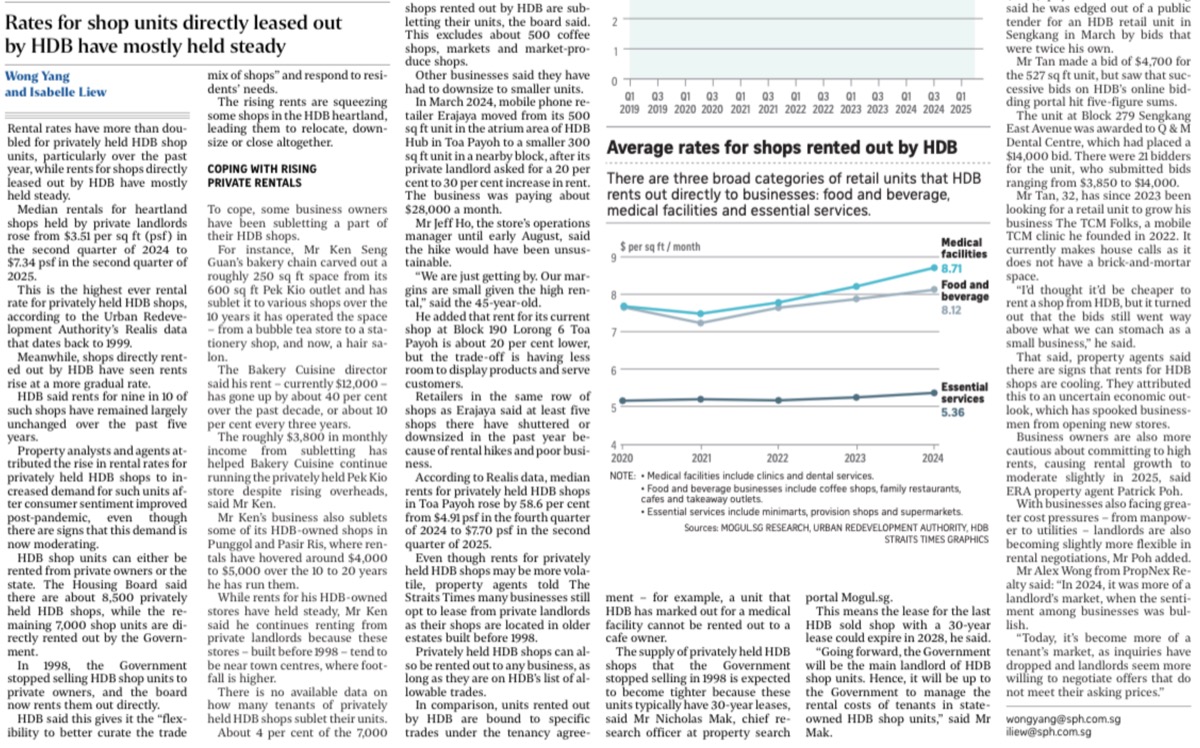

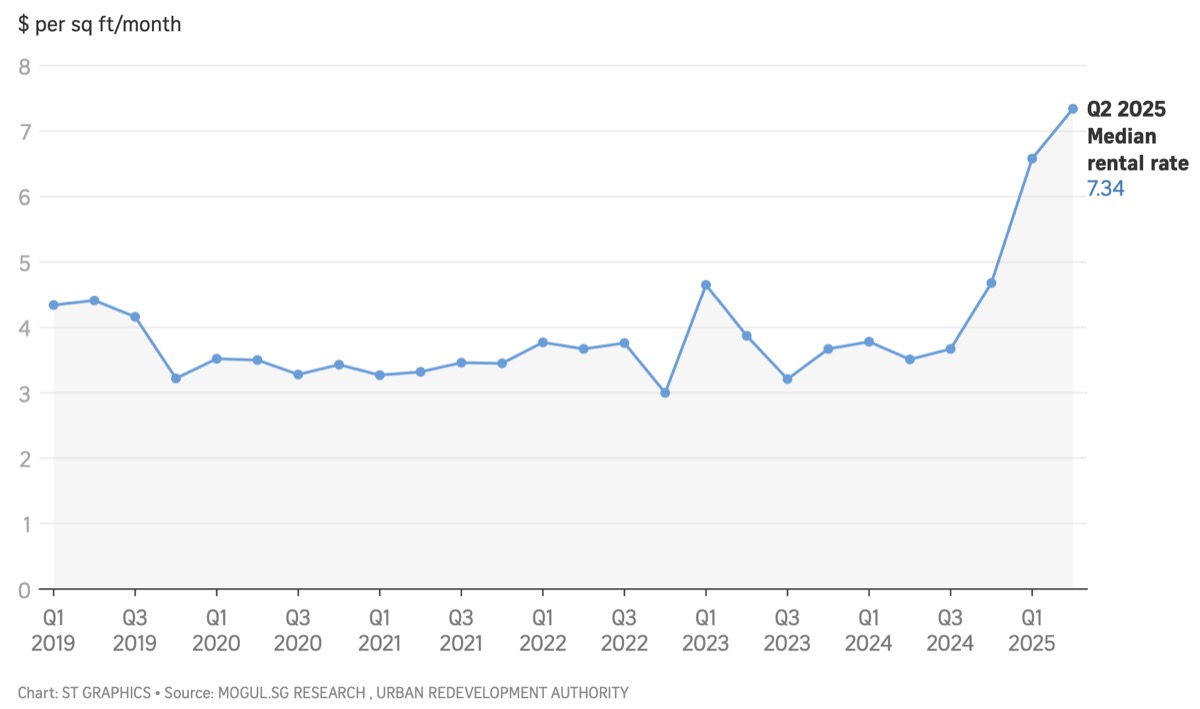

Heartland Rents Surging: F&B Tenants Face 30% Hikes as Shophouse Investors Pile In

Rent in the heartlands is getting pricier and choppier. Recent reporting shows privately-held HDB shop rents roughly doubled year-on-year while HDB-leased shop rents stayed steadier (Straits Times). On the ground, F&B operators describe ~30% renewal jumps that can flip a viable outlet into a loss-maker (CNA Talking Point). This piece is a quick read on what’s happening and how to price risk.

The Spike: What’s Happening Now

- Private landlords of HDB shops are asking a lot more at renewal; tenants report step-ups around 30% and, in some cases, sharper.

- HDB-leased shops (rented directly from HDB via tender) look comparatively stable, so the pain is uneven across the market.

- Shophouses and strata retail in mature heartland clusters are seeing strong interest from yield-seeking buyers, which pulls asking rents up.

- Bottom line: spreads looked great in 2024; 2025 feels more tenant-driven and selective.

Why It’s Up: Four Key Drivers

- Capital rotation into commercial after years of tighter residential cooling—more money chasing fewer bite-size retail assets.

- Structural scarcity: HDB stopped selling most new shop units long ago; older stock dominates and good frontages are rare.

- Post-pandemic footfall recovery in dense estates (convenience retail, F&B, medical), lifting revenue expectations for ground-floor space.

- Yield targets anchoring landlord asks—especially on recently traded assets where buyers underwrote higher rents.

Money Flows: Local vs Foreign Buyers

- Conservation shophouses and many commercial-zoned assets are generally open to foreign investors (check zoning and approvals).

- Heartland strata retail within HDB estates tends to be a local-owner market; but demand from family offices and syndicates still sets tone.

- Investor takeaway: financing, stamp duties, and zoning vary—confirm what you can buy, how you can use it, and whether F&B is a permitted trade.

Investor Math: Yield, Vacancy, Turnover Rent

- Work from net yield, not just headline psf. Add realistic vacancy and fit-out amortisation.

- For F&B, consider turnover rent or stepped rent to balance landlord yield and tenant survivability.

- Run a quick stress test: +20–30% rent at renewal, +10–15% payroll, +5–8% utilities—does DSCR still clear?

- Compare private asks against HDB tender outcomes nearby to sanity-check over-optimistic rent assumptions.

Conclusion: How to Play This Market

Rents in privately owned heartland shops have moved faster than many tenants can absorb, while HDB-direct leases remain comparatively steady. For investors, that divergence is the signal: underwriting needs to start from conservative, tenant-survivable rents rather than last year’s peak psf.

Focus on units with workable exhaust, grease traps and power so your tenant’s fit-out cost does not erase your yield. Be honest about the land-lease tail on older titles, because shorter tenure tightens lending and narrows your exit pool. If you are buying with aggressive rent assumptions, pair them with structures that give tenants breathing room—stepped or turnover rents often keep occupancy and cash flow intact. Finally, always price your deal against nearby HDB tender results and real vacancy risk.

In 2025 this is less about squeezing the last dollar and more about holding a stable, income-producing asset you can resell.

View Larger