Singapore's Rising Income: A Tale of Better Numbers But Heavier Wallets?

In CNA’s latest stats, provided by Department of Statistics Singapore, let’s talk about money.

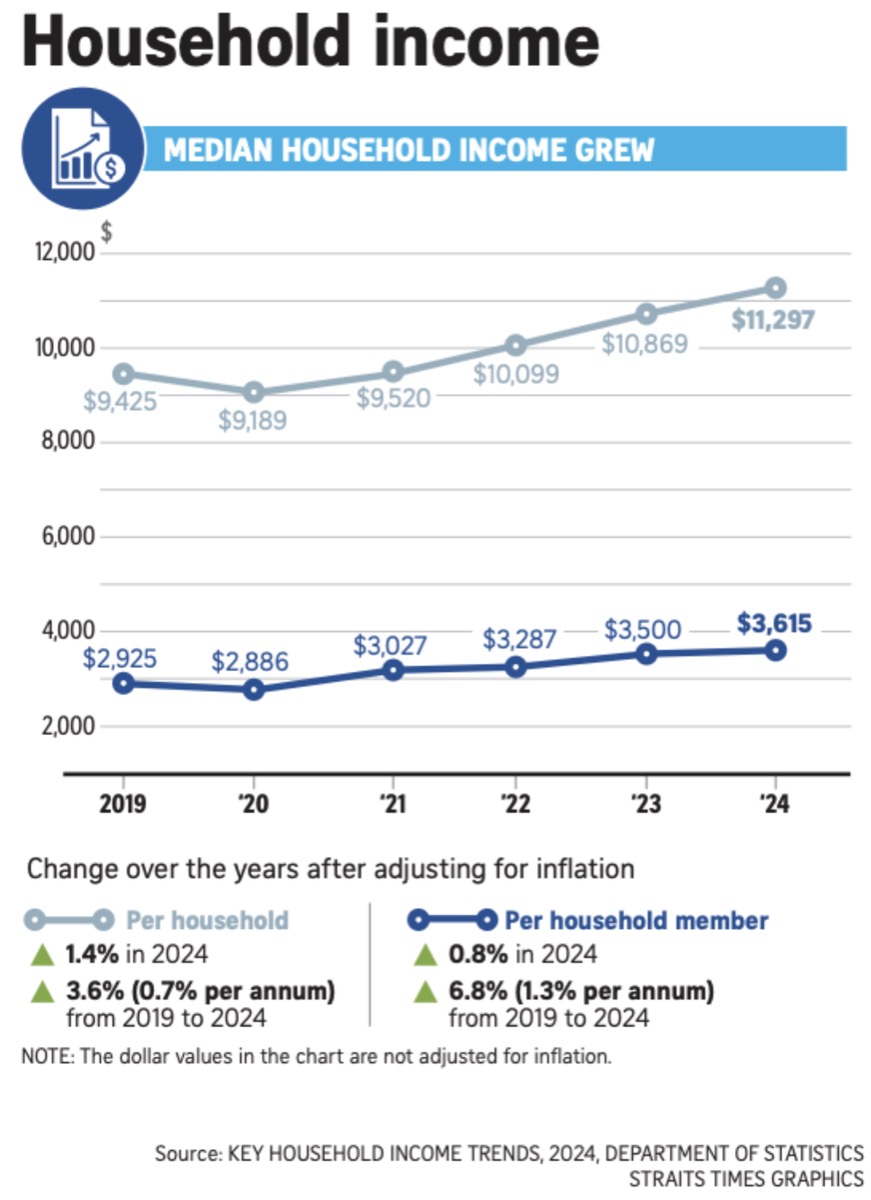

Specifically, that shiny new median household income figure that just dropped. Spoiler alert: We’re looking at $11,297 per month in 2024. Sounds pretty sweet, right? Well, grab your kopi and let’s break this down in true heartlander style.

First off, yes, that’s a 1.4% increase after inflation compared to 2023. But here’s the thing - it’s like when your boss gives you a smaller ang bao this year compared to last year’s. The growth has actually slowed down from 2023’s 2.8% bump. Not exactly the glow-up we were hoping for, eh?

Now, let’s get real about what these numbers mean for your property-buying dreams. If you’re thinking about that fancy condo or even a resale flat, here’s the tea: That median income of $11,297 might sound like a lot, but let’s do some quick math that your property agent won’t tell you about.

With the current TDSR (Total Debt Servicing Ratio) rules, you can only use 55% of your monthly income for all your loans. So for our median household, that’s about $6,213 to cover your home loan, car loan, credit card bills - basically everything that makes your bank account cry at night.

But wait, there’s more tea to spill! A savvy Redditor pointed out something interesting - we’re looking at household income, not individual income. So that $11,297 could be coming from multiple family members working their socks off, or even pulling overtime shifts that would make your grandmother tsk-tsk in disapproval.

Breaking it down further, a household member median income is $3,615.

And here’s the real kicker - while we’re celebrating these numbers, the government’s actually had to increase their support. In 2024, households received an average of $7,825 per member in government transfers, up from $6,418 in 2023. Those living in 1-2 room HDB flats got even more support - about $16,805 per member. Read between the lines, folks: If people need more support despite rising incomes, something’s not quite adding up in our cost of living equation.

The good news? The Gini coefficient (fancy term for income inequality) hit a record low of 0.364 after government transfers and taxes. The bad news? This might be painting a prettier picture than reality, since it doesn’t account for wealth from investments and other untaxed income sources.

So what’s the bottom line for property hunters? While our wallets might be slightly fatter on paper, the property market isn’t exactly rolling out the welcome mat for the average Singaporean. With property prices still doing their best Everest impression, that median income growth might just be enough to help you afford the downpayment on a new plant for your current home.

Remember folks, when it comes to property buying in Singapore, income is just one piece of the puzzle - and sometimes, it feels like we’re all playing a game of Monopoly where the bank always wins.

What do you think? Is your household income keeping up with your property dreams, or are you also considering a future tiny home movement?