Shoud you not take HDB CPF Housing Grant?

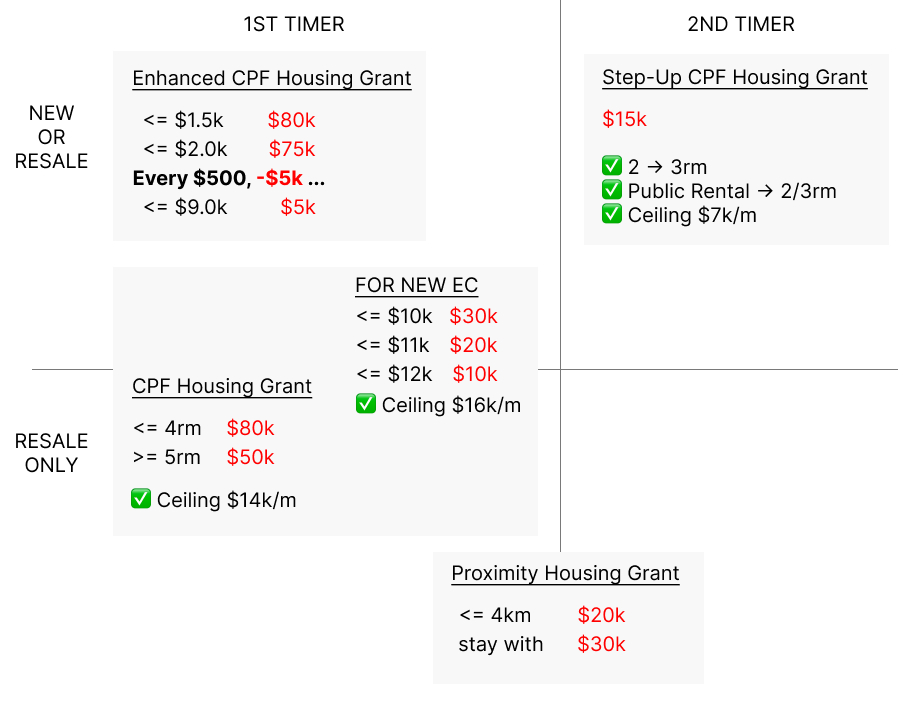

When buying a resale HDB, the government will support you by providing grant (aka free money), and the amount varies depending on your salary. It can be quite complicated, so here is a diagram. You can get up to $160k grant (if salary $1,500/mth)!

But some buyer might choose not to take up the grant, and some are rather misguided with their reasoning, and so this post is to clarify some of misunderstanding.

Myth: You have to return the grant

When you eventually sell the HDB, some claimed you have to “return the grant”, plus CPF accrued interest. That’s not quite true.

Here’s how the grant works.

Say you can get $50k grant. The government will give you this money by putting it in your CPF account, and then you can use it to pay for the property. Why not give you cash? Because the government wants it to be locked for property use only.

When you sell the HDB in the future, the sale proceeds has to be put back into your CPF account (plus accrued interest). You can’t call that as “returning”, because it is still your CPF money, and you can use it for the subsequent property purchase. Or if you are retiring etc, then it can be withdrawn or put in CPF Life.

Basically, it is still your money, just locked in CPF.

Myth: But there is interest

CPF has a 2.5% interest, and that is fixed for many years. It is sort of the risk-free interest rate.

The interest is fair, because there will always be inflation.

You have to judge based on the interest rate environment. If you have a $50k grant and choose not to take it, that means you are either going to use $50k cash, or to take additional $50k mortgage.

If you have $50k cash, then the better way is to find a risk-free investment that can earn more than 2.5% – that is not hard as current SSB/Tbill is at 3% (as of early 2025). You make a profit with the difference!

If you choose to take a $50k mortgage, then at minimum the interest is 2.7% (as of early 2025), and that is higher than CPF.

Ok, one might argue interest rate can go down. If that happens and you can’t beat CPF interest rate, then you can return the CPF with your cash, anytime. With cash, you can decide what to do. Cash gives you liquidity, cash is king.

Resale Levy

The biggest valid reason why one might not take the grant is the resale levy. The resale levy is one of the most complicated rule, and some buyers didn’t know about it until it hits them.

HDB defines subsidised flat as a new BTO or a resale HDB with CPF Housing Grant. One can purchase at most 2 subsidised flats in their lifetime, but a levy is placed on the 2nd purchase, based on the 1st flat type.

| Based on 1st flat type | Households Levy Amount |

|---|---|

| 2-room | $15k |

| 3-room | $30k |

| 4-room | $40k |

| 5-room | $45k |

| Executive Flat | $50k |

| Executive Condo | $55k |

For singles, the levy is half of households.

It is a simple fixed amount based on how many rooms (doesn’t matter the price, age, location, grant).

So if you plan to buy another BTO..

Then when you sell your 1st subsidised HDB, you will be hit with resale levy, and it can be hefty. You have to judge if the grant is worth taking vs the levy.

Why impose the levy? That is because BTO is priced cheaper, with a subsidy equivalent to a grant. HDB won’t want to give you discount twice, hence it imposes a levy to take back some.

Some examples:

- You bought a 5-room and got only $10k grant, yet the levy is $45k. Clearly you pay back more than you took.

- You bought a 3-room and got $50k grant, so the levy is $30k. When you pay the levy, you’re still net gain $20k.

If you decided the levy is too much vs the grant taken, then you can don’t take the grant in the first place, hence it won’t be considered a subsidized flat.

Conclusion

You have to make your own judgement considering how likely you’re going to buy a BTO in the future. If you’re never going to buy another BTO, then clearly you should just take the free money.

The resale levy rule might even change in the future. Who knows.

{kind=link}