The key to finding your perfect property should be in your hands. We empower you with valuable insights & tools, and let you be in control of your home search.

RES Course

Competency Unit 4B - HDB

Sale of HDB

Seller submit Intent to Sell

Wait for 7 days cooling period

12m validity

Buyer apply HDB Flat Eligibility (HFE) letter

Eligibility for New/Resale, CPF Housing Grants, HDB Loan

Consider 12m income, ending 2m ago

Must be working

6m validity

Buyer must comply with

Ethnic Integration Policy

SPR Quota Policy

Max non-Malaysian PR, neighbourhood 5% and block 8%

SPR need status > 3y

If sell private

Wait out 15m if w/o CPF Housing Grant

Exception for > 55yo moving to 4rm

OTP (read below)

Using CPF, must Request for Value

Extension of stay up to 3 months

Sale Proceeds

Pay bank outstanding first

Then CPF to return plus accrued interest, housing grant

If not enough, no need topup shortfall

Resale inspection: check for unauthorized

Must fix before completion

OTP

Only HDB prescribed OTP

Deposit max $5k, the norm:

Option Fee $1k (max $1k)

Option Exercise Fee $4k

Min $1 to be valid

Buyer pay option fee in cheque

Option expire 3 weeks, 4pm

During which can apply bank’s Letter of Offer

To exercise, buyer has to sign the Acceptance, deliver, pay in cheque to seller

Seller can authorize agency/law firm to receive

Agents/lawyers cannot receive cash, so must be cheque

Agent can be witness

Use of CPF

Lease > 20y

Can use max OA

If can cover until youngest buyer 95yo

If not, pro-rated

The most complex of all.. try decipher CPF or their FAQ

Formula? (Lease - 20) / (95 - 20 - youngest)

Resale Levy

A subsidised flat is:

New or

Resale with CPF Housing Grant

Max 2 subsidised flats

A levy on the 2nd purchase, based on the 1st flat type

Based on 1st flat type

Households Levy Amount

2-room

$15k

3-room

$30k

4-room

$40k

5-room

$45k

Executive Flat

$50k

Executive Condo

$55k

For singles, the levy is half.

Eligibility

The Schemes:

Public: family

SC + PR

PR + PR (both at least 3y)

Fiance

Single

35yo

New: 2rm flexi

Resale: Any

Joint Single (up to 4)

Non-citizen spouse

Non-citizen family

Orphans: with siblings

Income Ceiling

New:

3rm or smaller: $7k

4rm or bigger: $14k

3Gen: $21k

Resale

Grants

Both New & Resale:

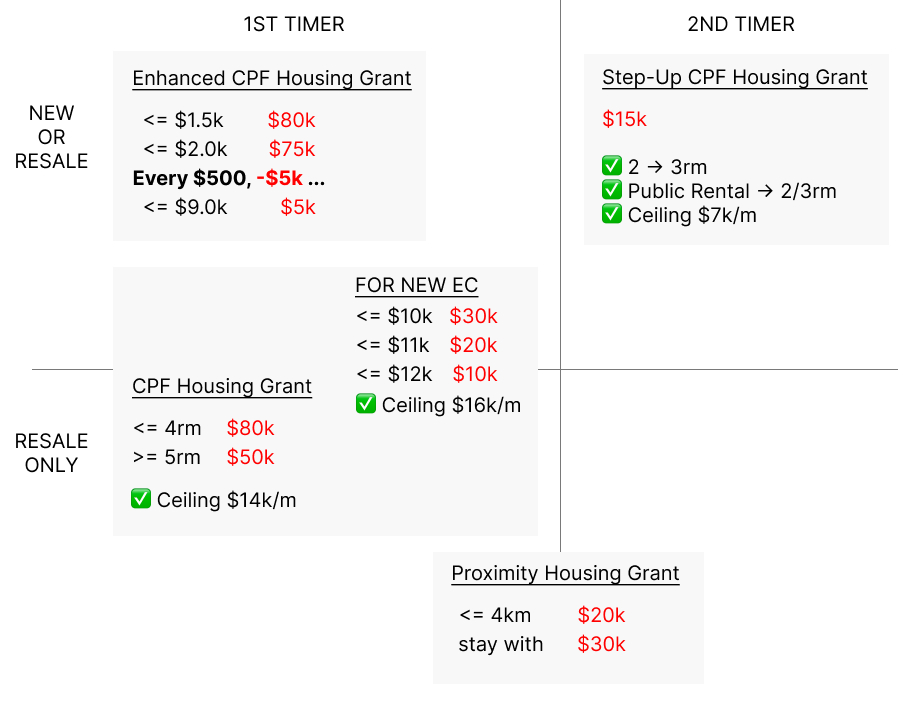

Enhanced CPF Housing Grant (1st timer)

Step-Up CPF Housing Grant (2nd timer)

Resale only:

CPF Housing Grants (1st timer)

Proximity Housing Grant (1st & 2nd)

For single, half the family grant, half the ceiling

If household is SC + PR, there is -$10k (when has citizenship, can apply citizen top-up)

Income ceiling applicable for new, while resale only affects the grants

Enhanced CPF Housing Grant

Household Income

Family Grant

<= $1.5k

$80k

<= $2k

$75k

<= $2.5k

$70k

…

…

<= $8.5k

$10k

<= $9k

$5k

Memorize first row, then every +$500 income, -$5k grant, until $9k no more grant.

At least 1 worked for 12m

Lease must cover up to 95yo, if not pro-rated

Step-Up CPF Housing Grant

Upgrade from 2rm -> 3rm

Or Public rental -> 2/3rm

Income ceiling $7k

At least 1 worked for 12m

Grant $15k

CPF Housing Grant (Resale)

HDB 2-4 rm

$80k

HDB >= 5 rm

$50k

Household income ceiling $14k

Remaining lease > 20y

CPF Housing Grant (New EC)

Income <= $10k

$30k

Income <= $11k

$20k

Income <= $12k

$10k

Household income ceiling $16k

Proximity (Resale only)

Parents < 4km

$20k

Live with parents

$30k

Does NOT consider income ceiling

HDB Loan

HDB loan is NOT subsidised housing; It is an entitlement

Income ceiling

Household $14k

Single $7k

For 2nd HDB Loan, reduced up to half of cash proceeds

Means must use 50% of cash proceeds for 2nd purchase

GREATER $25K POLICY

Cash proceeds can only keep max($25k, 50%)

If want keep all, don’t take HDB loan

HDB Shophouse

1st level commercial

2nd level residential

Considered a commercial property, but account for residential portion

Can own 1 HDB + 1 Shophouse, but must pay ABSD

Pay ABSD for the residential portion only

Pay BSD for commercial + residential portions accordingly

Foreigners can buy too, but if zoned for residential must approve by LDAU

Standard vs Plus vs Prime

Standard

Plus

Prime

Location

Islandwide

Choicier

Choicest

Subsidies

Standard

More

Most

Subsidy Recovery

No

Yes

6% of resale

MOP

5y

10y

10y

Rent out whole flat

After MOP

❌

❌

Wait-out for private

15m

30m

30m

Additional conditions for Plus & Prime resale flat:

Household must have SC

Income ceiling $14k

2-rm Flexi

For more than 55yo

Can lease 15-45y, as long as cover until 95yo

Income ceiling $14k

Previous 2 subsidised housing does not include studio/2-rm flexi/CCA

Similar to 2-rm Flexi, but:

More than 65yo

Can lease 15-35y, as long as cover until 95yo

Senior friendly

Silver Housing Bonus

When selling property (AV < $13k) to buying 3-rm or smaller

Topup RA $60k -> Get cash $30k

BTO Balloting

2nd-timer 1 chance

1st timer

2 chances

3 chances if FT(PMC)

Has a SC child < 18yo etc

+1 for every unsuccessful, after 2 unsuccessful, only for non-mature eg. For 3rd application, +1, 4th +2

Non-selection

Become “2nd-timer” status, clear all those additional chances

Many Priority Schemes

Can choose up to 2

Set aside quota

Decoupling

Restrictions Against HDB Decoupling From 2016, MMDDFL:

Marriage

Medical Grounds

Death Of An Owner

Divorce

Financial Hardship

Loss Of Citizenship

Rental

Tenant pays Stamp Duty, unless stated otherwise

Landlord pays Property Tax & Conservancy fees

Expense

Allowable: Mortgage repayment, property tax, fire insurance, repair, etc

HDB Rental

PR or under MOP cannot sublet whole flat, but bedroom OK

Non-malaysian Non-citizen (NC) quota for whole flat

Max Neighbourhood 8%

Max Block 11%

Work Permit holders from the construction, marine, and process sectors must be Malaysians

Work Permit holders from the manufacturing sector must also be Malaysians, if renting whole flat

Min lease 6m

Only >= 3rm can rent out bedrooms, and the max number of occupiers (including owners) is the same as sublet whole flat

Sublet Flat

Max unrelated occupiers

<= 2rm

4

3rm

6

>= 4rm

8

Private Rental

Sublet Private

Max unrelated tenants

< 90sqm

6

>= 90sqm

8